What is International Financial Service Centre (IFSC)?

How is an IFSC regulated?

Who are the participants in an IFSC?

The participants in an IFSC are as follows:

What is the key difference between an IFSC unit and a domestic unit?

What does the IFSC mean to the global fund managers?

How are the funds regulated in IFSC?

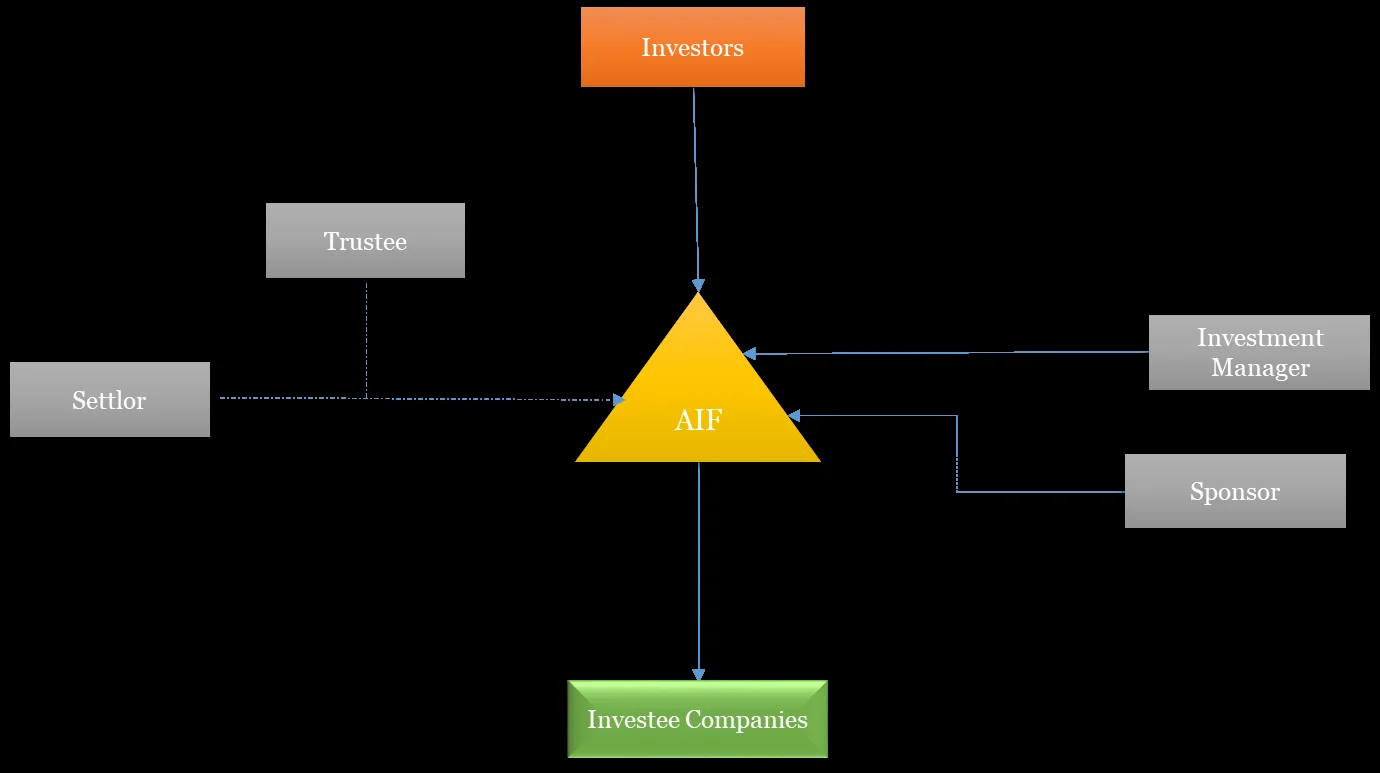

How does an AIF operate?

Operational structure of an AIF: